Inside the money game

As an author, investor, podcaster and teacher, two themes have been central to my professional life – investing in the stock market and the game of bridge. Participating in them, talking about them, writing about them, giving advice about them – if you are interested in either, you can find out more here. This is my professional website.

Professional life

Investment expertise

Practitioner

After an early career in financial journalism, and columns for the Independent and Financial Times, my professional investment life began with a year at MIT’s Sloan School of Management where I met and wrote a thesis about the investment methods of Warren Buffett for a Master’s degree. More recent commitments include wealth management positions with Smith & Williamson and Saunderson House, independent consultancy work and editing the Money Makers website (podcasts and market commentary).

Author and analyst

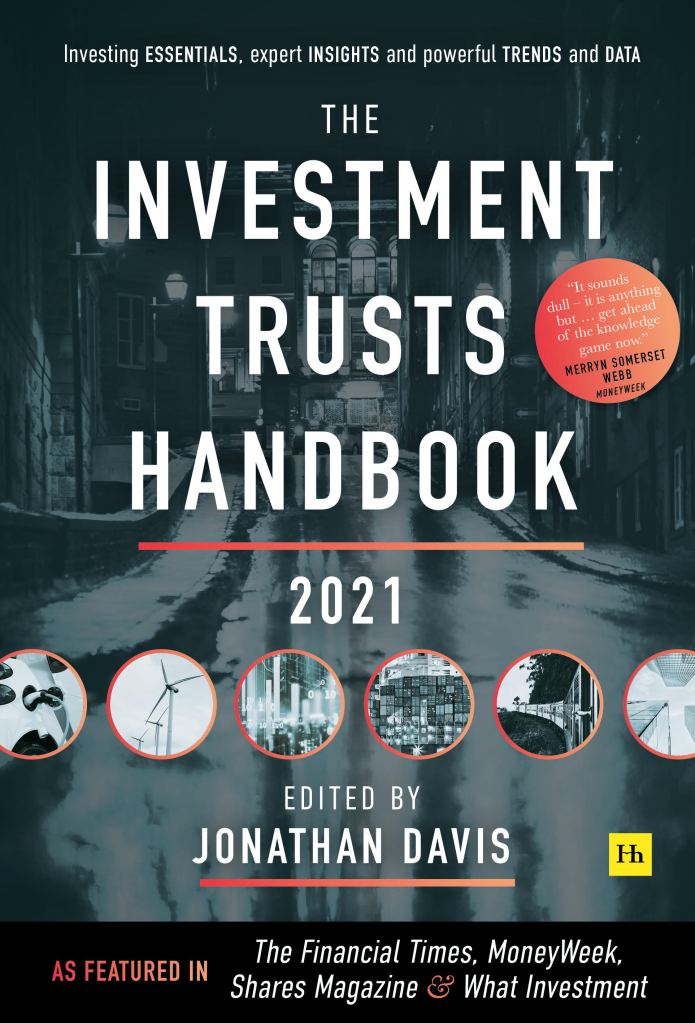

In a joint venture with the financial publishes Harriman House, my work includes both writing and commissioning expert books on investment themes. These include the annual Investment Trusts Handbook, which has reached more than 45,000 readers and is now in its sixth edition. The latest edition was published in December 2022. The next will be out in December 2023. A fuller list of titles, including the books written by myself and other professional investors, can be found on the books page.

Podcaster

My free weekly investment trust podcast offers listeners a ringside view of the financial markets and what Keynes called “the game” of stock market investment. It is a weekly discussion of the latest news and trends in the investment trust world with a range of professional experts. New listeners are always welcome. We regularly obtain more than 3000 listeners a week. The podcasts are independently produced and edited. Premium Money Makers content is also available in return for a modest annual subscription.

Teaching the world about a great game

Bridge in Oxford

200+

followers

10

weekly coaching sessions

11

courses

25

weekly seminars

Sharing knowledge

My books include three titles analysing the success of those few professional investors who – in an age dominated by the rise of indexing – can genuinely be said to have added value for those who buy their funds.

- Money Makers

- Templeton’s Way With Money

- Investing With Anthony Bolton

For other commissioned titles, click here.

Sample columns from the past 20 years

From the archive

- Is it virtue or results that you want?I am a fan of Terry Smith but I wonder how many others in the fund management business are, given his knack of puncturing some of the carefully-developed myths that help to keep the rest of the industry going. His latest offering. a “sustainable” global equity fund, is a clever and well-judged attempt to highlight the flaws in the way that many other funds in this fashionable sector are in practice put together.

- Governments are dumb about propertyI have recently started a series of interviews with leading figures in the property world for a new specialist publication The Property Chronicle. This month’s subject is David Lewis, a well-known property developer whose interests over a 40-year career included three listed companies and a range of private ventures. He looks back on his highs and lows, gives his views on current market valuations and expounds on his view that Governments rarely make a success of their interventions in the property market. The first interview in the series was with Professor Andrew Baum of Oxford University, a leading property academic (yes there are such things) and a pioneer in property market research. He also has a fair bit to say about the challenges of valuing property in a low interest rate world.

- Another cheap and cheerful milestoneWhile active fund managers are getting active, as they have to do to justify their existence, the announcement that Vanguard, the pioneer of low cost index funds in the United States, is entering the platform market in the UK for the first time, offering